I'm sure there is a downside to this which I haven't considered, but it's a viscerally compelling argument. I like it. BTW, I lived in a country where 10-15% retail discounts for payment in cash were common and it certainly made me think twice about using plastic. (I was told that global credit card banks were lobbying the government to outlaw the practice, no big surprise if true.) Of course, the author assumes consumers have the financial wherewithal to pay in cash, and especially in this recession, many do not.

A Simple Plan to Screw Big Banking. Use Cash.

By Chaz Valenza

November 28, 2009 | Chaz Valenta

Here's a simple plan that will bring Big Banking to its feet: Use Cash.

For decades Big Greed has been selling us the idea that markets are just perfecto! Don't regulate them. Don't even bother chasing down fraud. "The Market" (Angelic Voices: Ahhhhh!) is so beautifully simple even scams cannot long survive.

Let's take the "Wisdom of The Market" stick it up Big Banking's rectum, twist, turn and otherwise shove vigorously and often.

Face it, the cavalry is not coming to the rescue if your name is not Goldman Sachs.

Government of the people, by the people, and for the people is temporarily out-of-order, like a soda machine that is taking dollar bills from customer after customer but relinquishes not one quenching 12 oz. can.

No legislation or regulations are in the offing to cap the rising tide of usury interest rates, curb punishing banking fees on debit cards or curtail demonic payday loans.

Here's the bill of fare:

Credit Card Interest: 30%

Merchant Credit Card Fees: 3.5 - 5%

Merchant Credit Card Receivables Loan: 36 – 97%

Payday Loans: 100 – 500%

Debit Card Overdraft Fees,

Over limit Fees, Late Payment Fees, etc:

Interest Equivalent to 12% - 300% and otherwise unlimited

Throw stones – millions of them. Every plastic transaction denied is a slice in the skin of Big Banking.

As a buyer: Use Cash. It's going to save you money verses paying with credit card or making a mistake with a debit card.

As a merchant: Discount 5% for Cash. It's going to save you money in reduced merchant charges and days waiting for credit card receivables. It's also an advantage against the Big Box stores and Big Food restaurants.

Think about it. Who would you rather have that 3.5% you give to Big Plastic on every credit or debit card transaction: Your customer or Big Banking? Isn't that worth the extra 1.5% in the discount?

But it gets better. It's guerilla warfare. It's a simple insurgency. Avoid the banking system to bring it to its knees. Use Cash.

How low-tech is this? How unstoppable? How inconvenient? Yes. But worth it!

Put it on bumper stickers. Make it your email signature. Pass the word in whispers to everyone who works for a living. Write it in magic marker on T-shirts. Design a flag and boldly embroider. Print up window signs. Post it on every blog you visit. Tweet it from the highest mountain. Two simple words: Use Cash.

Will they fight back? Of course they will. They will end Absolutely Free* Checking that is costing us all billions. They may lower their rates and switch up the penalty fee structure. They might even lobby for the end of printed dollars. That's how we'll know it's working!

Here's the future and the future is now. Personal loans? Small business lines of credit? Only to those who don't need them or at a killer rates of interest.

Use Cash.

Every cash transaction snatches a dime, a dollar, thirty-five dollars, a hundred dollars or more out of the greedy, blood soaked hands of Big Banking. Each transaction denied is a cut. Together it's death by a billion cuts daily.

5% Discount for Cash.

You'll be shooting at Big Plastic's feet. Smile as you watch 'em dance. They have us hooked on plastic. They claim it's faster, quicker, better. People spend more. Yes, they do. Until the abusive fees take your customers' last penny of discretionary cash and they're broke.

Debit or Credit, plastic is really just one thing: a cash substitute provided by a commission taking broker who charges you a fee at every cash register. They intend to milk it for all it's worth. Cut up your cards, today, right now.

And here's the beauty part: We don't need no stinking badges to fight back. Just: Use Cash. Wow! I'm starting to agree: The Market Rules!

Don't worry about freeing up credit or ending the banking abuse, etc. This is action you can take right now, and again and again, day after day after day.

Sure, there are bigger fish to fry: End the Fed, local currency, non-profit banking, total monetary reform, but this is something we can do right now.

It's easy, fast, effective: Don't give Big Banking any small change.

Yes we can nickel and dime the banks to death! Spread the word: Use Cash.

Chaz Valenza is writer and small business owner in New Jersey. He earned his MBA from New York University's Stern School of Business.

Sunday, November 29, 2009

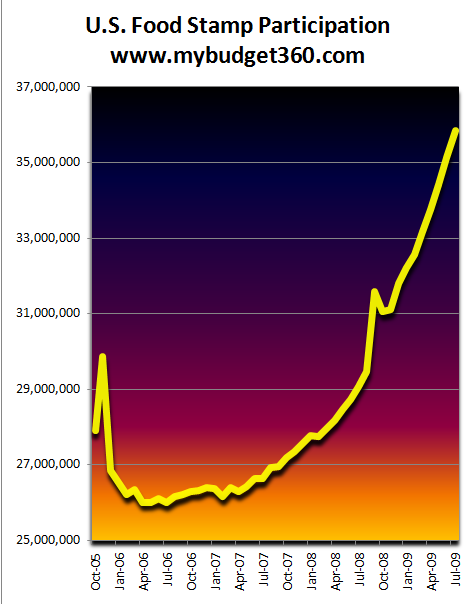

Thanks, Obama: 12% of Americans on food stamps

Look what BHO has reduced us to: 1 out of 8 Americans is a helpless welfare junkie dependent on gov't cheese.

Meanwhile, the states, like drug dealers, are pushing food stamps on more and more erstwhile honest, hard-working, self-sufficient Americans, because unlike cash welfare payments, food stamps are 100% federally funded.

Even conservative and once proud Warren County, Ohio, which turned down federal stimulus funds on principle, has lately doubled its dependence on food stamps. Said proud, principled, Warren County Commissioner Dave Young [R]: "As soon as people figure out they can vote representatives in to give them benefits, that's the end of democracy. More and more people will be taking, and fewer will be producing." You tell 'em, Dave! ... I mean, wait! Don't tell them! You just helped the people figure it out! Nooooooo!.....

Seriously though, the following excerpt so neatly encapsulates everything that's wrong with white, middle-class, conservative Americans, who are getting beaten over the head by economic forces they can't control and yet oppose any programs or reforms designed to help them or their compatriots:

While Mr. Dawson, the electrician, has kept his job, the drive to distant work sites has doubled his gas bill, food prices rose sharply last year and his health insurance premiums have soared. His monthly expenses have risen by about $400, and the elimination of overtime has cost him $200 a month. Food stamps help fill the gap.

Like many new beneficiaries here, Mr. Dawson argues that people often abuse the program and is quick to say he is different. While some people "choose not to get married, just so they can apply for benefits," he is a married, churchgoing man who works and owns his home. While "some people put piles of steaks in their carts," he will not use the government's money for luxuries like coffee or soda. "To me, that's just morally wrong," he said.

He has noticed crowds of midnight shoppers once a month when benefits get renewed. While policy analysts, spotting similar crowds nationwide, have called them a sign of increased hunger, he sees idleness. "Generally, if you're up at that hour and not working, what are you into?" he said.

Note how even as he receives welfare, he can't overcome his hardwired angry-white-guy programming to criticize other people on welfare. Classic.

The Safety Net - Across U.S., Food Stamp Use Soars and Stigma Fades

By Jason DeParle and Robert Gebeloff

November 30, 2009 | New York Times

URL: http://www.nytimes.com/2009/11/29/us/29foodstamps.html?pagewanted=1&_r=2&th&emc=th

Mark Pittman (RIP) on mortgage crisis, Fed

Audit Interview: Mark Pittman

By Ryan Chittum

February 27, 2009 | Columbia Journalism Review

By Ryan Chittum

February 27, 2009 | Columbia Journalism Review

(UPDATE, November 29, 2009: Mark died a couple of days ago. It's a huge loss and we'll have more on him next week, but until then you can read some of what we've written about his exploits here. We wrote about when he and Bloomberg sued the Fed and when he won. Here's Pittman with his friend and colleague Bob Ivry (who wrote Pittman's excellent obituary), with a great profile of Elizabeth Warren last week. Here's our look at how a Pittman story last September helped break the huge story of Goldman's (and others') backdoor bailout through AIG.

Here he is going after an incredibly complex story: How much are those toxic assets actually worth? And Pittman kept a close eye on the disastrously bad deals Uncle Sam cut for itself to benefit Wall Street. Watch him leverage the hot story, the AIG bonuses, to show how much bigger another story was, the bailouts of AIG's counterparties.)

Mark Pittman has been all over this financial crisis.

He was part of a team at Bloomberg News that won the Loeb Award last year for a five-part series on the origins of the crisis called "Wall Street's Faustian Bargain," including Pittman's lead story on how the Street goosed the subprime mortgage market late with financial engineering.

The new standardized contracts they created would allow firms to protect themselves from the risks of subprime mortgages, enable speculators to bet against the U.S. housing market, and help meet demand from institutional investors for the high yields of loans to homeowners with poor credit.

The tools also magnified losses so much that a small number of defaulting subprime borrowers could devastate securities held by banks and pension funds globally, freeze corporate lending, and bring the world's credit markets to a standstill.

In addition to the Loeb-winning work, Pittman has broken major stories on Goldman Sachs's interest in the AIG bailout, Hank Paulson's role in creating the subprime mess, and the ratings agencies inexplicable delays in downgrading mortgage securities, and he's delved into how Wall Street spread its detritus across the world.

Pittman is a native of Kansas City, graduated from the University of Kansas, and got his first job covering cops at the Coffeyville Journal in southern Kansas, where he was paid so little he had to get a part-time job as a ranch hand across the Oklahoma border in Lenapah. Proving yet again that it really is a small world and journalism is even smaller (and getting smaller every day, as Pittman points out) we discovered to our amazement that my late grandfather Arva Chittum was a good source of Pittman's back in the early 1980's in Coffeyville.

He spent twelve years at the Times Herald-Record in Middletown, New York, before joining Bloomberg News in 1997.

We spoke recently about cops, CDO's, and the crisis.

The Audit: How did you get started at Bloomberg News?

Mark Pittman: That was back when Bloomberg News only had like fifty people in New York. I covered oil in the beginning and then they moved me to covering securities firms. I was covering the Street in 1999 to 2000. There were only two of us covering the whole Street. We didn't do a very good job as you can imagine. We could barely get the earnings out.

I went on to private equity and corporate finance. I got a wide education. I learned a lot about trading. If you cover the oil markets, those guys know how to trade. They know how to pull the trigger on stuff and back out. That gets in your bones. When you realize how you make money doing that kind of stuff, a lot of other things make sense. I'm not sure that a lot of business journalists get that kind of knowledge.

That's stuff you just don't get covering companies or doing profiles. You learn different stuff.

TA: How'd you get onto the crisis story?

MP: I had a conversation with a couple of people in late 2006/early 2007, and people were talking about what's wrong with asset-backed securities and where all this is headed. I'd also covered derivatives contracts. When they first started doing credit-default swaps on companies, I covered that. That was like '99-2000. You could tell it was going to be a really hot thing.

When they started talking about doing derivatives on mortgage-backed securities [a bet against the housing market; this is explained a few lines below], I was like "oh, man, that means the banks are scared!" That was 2006, and we wrote a whole series about this.

You always want to be around the hot story. If you're not around the hot story, you're screwed.

TA: So did you go into that pretty much full-time? How'd you convince your editors to let you do that?

MP: You know it really wasn't hard. They've really let me take a lot of chances here, and they're extremely generous with my time. They recognize it as an important part of the reporting process. They give me a lot of rope. They let me figure stuff out. That's something that's in real short supply with a lot of news organizations now. You've got to let reporters run and figure out what's going on.

TA: Not many others have the resources to do much of that nowadays.

MP: Instead of doing the sixth sidebar on a bailout program that probably won't work anyway, let the person figure out what's actually happening. And you've got to let your people do that.

We did a five-part series [the one that won the Loeb] on the whole idea of why the subprime crisis occurred, and it starts with this story about how a bunch of traders at Deutsche Bank, Goldman Sachs, JP Morgan got together and said "We need a standard contract to be able to short the mortgage market." As soon as I realized they were going to try and short the mortgage market I said, "Ohhh. That means they think the market is going down."

TA: And these are the guys who've come out pretty okay in this.

MP: You'll notice UBS and Merrill aren't in the group. The thing about this entire series of events is this is so complicated and so intertwined that we don't have —journalists are not qualified to cover the story. We don't have the background. These guys are doing stuff that you had no idea was happening. The off-balance-sheet accounting stuff is crazy.

TA: Well, if the ex-chairman of the Fed Alan Greenspan, formerly regarded as a near god, didn't understand what this stuff was, who did? He had access to all the people and all the information he could want.

MP: He had no idea what was going on. How is it possible for them to sell themselves, to an off-balance-sheet entity, risk that is now exploding all over everybody? Why would that be allowed and why would you be able to book a profit on this? Who was in charge of this?

We haven't got to the bottom of this whole thing yet. Somebody's going to do this big forensic—and it might be me!—somebody's going to do the deep dive into how everything happened and they're going to find out that this system was just on autopilot and was spinning money out to a whole bunch of people. And it included you and me.

TA: In the form of cheap credit?

MP: Yes. The spreads should never have gotten to that level.

This goes back to why AIG is all screwed up. The banks sold AIG all their risk in 2007, when it was really blowing up. AIG had sworn that they weren't going to do any more of this and then (the banks) restuffed the CDO's [collateralized debt obligations] with new stuff. So (AIG) had newer collateral that they weren't really aware of.

TA: So the banks were stuffing the CDO's with new stuff but AIG didn't know they were replacing the stuff?

MP: Right.

TA: An MBS [mortgage-backed security], you can't move things in or out, but a CDO you can. Are the banks liable for this? AIG got blown up, but these guys knew what they were doing.

MP: You know what, the lawsuits will have to sort that out. And it's going to be going on for years. It's going to be just a debacle. Congress is going to have go through and force people to say "Okay, so what did you do with this, and where did it go from here?" They need to have very talented investigators go in and find out what the deal is.

TA: Tell me how your cops background plays into what you're doing now.

MP: You end up with a big BS detector as a cops reporter because the cops lie to you, the victims lie to you, the people helping the victims lie to you. And you've got to sort through and there will be a story that seems a certain way and it just won't be—and you know it. That's what this is about.

The reporters who didn't question the tight, tight spreads [the narrow difference in interest rates offered by Treasury bills and other, less secure instruments] that were going on in corporate [bonds], it was wrong. Where is this demand coming from? How can you guys sell this issue in thirty minutes? Who the hell's buying this stuff like that? We're going to come to the answer that it was going off balance sheet, at least temporarily, and then it might be sold to other customers.

TA: So they were buying it themselves and…

MP: They were buying it themselves. Yeah. And not every deal. But you know what—it happened enough. We don't have enough journalists in America who understand what a spread does, which is the essence of banking. I just finished Dean's piece in Mother Jones recently. We've got 9,000 business journalists and maybe twenty of them know what a spread is. This is not business journalism's finest hour. But it is our biggest opportunity ever.

TA: How does the Bloomberg terminal inform your reporting or help you find leads?

MP: Well, I'll give you an example. The first best story that I did about this—I'm gonna brag about this—was in June of '07. It said that subprime bonds are failing and they're failing at an alarming rate, and they're going up a lot, and they all need to be downgraded. The ratings companies aren't following their own criteria for what makes a bond a certain rating. I did that through data that's available on the Bloomberg. We've got a function called DQRP, which gives you delinquency reports on every RMBS [residential mortgage-backed security], dividing it up by category. So you can pick the worst bonds with the worst stuff and you can divide it up by rating—all kinds of sorting. Nobody has that but us.

TA: I didn't even know that capability was out there.

MP: Hell yes, man. And it works. Then you can pull up each individual bond and you've got a complete description of its geographic reach—how much is in California, all kinds of great stuff. What a weapon! And if you know how to use it, it works pretty well.

TA: So what's your prescription for business journalists? What do they need to know and do? Not everybody's going to have a $20,000 a year Bloomberg terminal to play with.

MP: Hardly anyone has a Bloomberg machine and the ones that do don't know how to use it.

But you know what? The government needs to make this kind of data much more publicly available than it is now. We purchase a lot of this. But, for instance, a lot of the bond deals were (not subject to disclosure). And all the CDO's were private placements. We know why—because they placed them with themselves. The number of secret deals going bad is astounding, it's probably 90 percent of them were secret deals.

TA: Bloomberg's got a ton of people on bonds, but I've said before that a part of why the business press failed here was that it has so many times more people covering equities than debt. And debt markets are many, many times the size of the equity markets. That's kind of a major problem right there, right?

MP: It is huge. Most reporters, it's shocking how few of them actually understand the difference between price and yield. Hardly any business journalist actually covers the financing. If you cover a company and all of a sudden their borrowing costs go from 100 (basis points) over to 250 or 300 over [meaning investors believe the risk has increased substantially], and no one asks a question. There's a problem there when that happens and nobody asks a question. I think we have training issues in a huge way in our profession. We brought a knife to a gunfight.

TA: Does there need to be regulation just to simplify things to where it makes sense to more people?

MP: If it was all transparent the complexity wouldn't matter. If the CDO market had had publicly available prospectuses with the contents of the CDO disclosed, we wouldn't have this issue, because Bloomberg probably would have made fun of anybody who bought anything like this. But there was this enormous shadow banking system going on. We did a series about that, too. A lot of times people don't see what we do.

TA: That's one of the problems I've noticed. We've consciously tried at The Audit to make sure people are reading your stuff. I don't think it's become a habit for a lot of people even in the biz to go over to Bloomberg.

MP: It kinda bums you out, because you want to do things that have big (impact) because that's why you're in the business. And public policy would work a lot better if they actually understood what the hell was going on.

TA: Like adding up the total number of trillions that the government is on the hook for in this bailout. Nobody else is doing that but you. Why not?

MP: Because it's a big pain. You start off with whatever you can remember off the top of your head—oh, they're doing this, they're doing that—you start writing it down on a piece of paper and you go "Wow, this is real money." It starts adding up.

The thing that people don't realize is that the Fed is now the "bad bank." That's just something that people don't understand. They've taken collateral, and they refuse to tell us how they valued it…

We have numerous banks— dozens, maybe hundreds that are insolvent. And they become more insolvent every day because more people quit paying their mortgage loans, and more guys move out of the shopping center, and more people quit paying their credit cards. But nobody wants to have the adult conversation…We need to be honest about what the problem is here, how big it is, and how we're going forward to clean it up, and who's going to pay for it.

TA: Basically the charade that's going on here is that they haven't marked these assets down yet because that would show they're insolvent.

MP: But a lot of [the assets] have gone to the Fed, though, as collateral for loans. They're still on their balance sheet, but you borrowed against them. We don't know if those are cracked CDO's or prime RMBS…

TA: That's what you guys are suing (the Federal Reserve) for—to find out what the collateral is.

MP: Yeah, and that's the secret part of the story that nobody wants to let you know.

TA: Because it's worth pennies on the dollar or dimes on the dollar.

MP: Yeah, and then everybody's going to go "Oh my God, we're lending ninety cents on something that's worth twenty or thirty?"

TA: They say they don't want to disclose it because it would interfere with the markets, is that right?

MP: Their basic argument is this would cause chaos, and they're probably right. But that doesn't mean that the American taxpayer ought to be on the hook for this.

TA: Why would it cause chaos?

MP: Because people would realize that we're lending eighty cents on the dollar for something that's worth twenty cents.

TA: So political chaos?

MP: And maybe market chaos, too. Well, you know the market's probably pretty savvy about this thing, and everybody knows what's going on but we just haven't communicated with the public. When you say "political chaos" you might well be right. That may be what it was. Congress is going to go "We're lending this much money on this Triple-C security? What are we thinking here?"

TA: One thing I really like about you guys is in your reporting and writing, you have a sense of outrage that's not in the Journal, say. This thing is so huge, and you guys are conveying the magnitude of it better than some, and there's a sense of urgency that's lacking elsewhere. Is this a conscious thing in the newsroom?

MP: We have been primary movers for transparency in markets since our existence. Bloomberg's reason for being was to give the buy side enough tools so they wouldn't get screwed by the investment banks. That's what we're about. So we're a weapon for the buy side and a de facto weapon for every one who has a mutual fund. We just need to level the playing field and let everybody know what's going on. This is from Matt Winkler on down. This is what we do.

It's also that we realize this is a defining moment for business journalism and for Wall Street. I think that this organization, this news department, was built for this crisis. We've got more tools than anybody, we've got the will, we have the assets to go after this in a huge way. Everybody believes that in this room.

Hopefully, we will be able to inform the people enough to know how badly we're getting screwed (laughs). We need to know how to prevent it from happening again, and we need to know who did it. There's renewed energy on this front because we've staffed up the people who cover banks, the securities firms. We have a lot more people going at real estate and a bunch of different areas that this involves. That was a conscious move from meetings we started having in 2007. We hired people and we moved people from one area to another area.

Our issue is we have readers who are very interested in very small things. That's why they have the terminal. It's because they're interested in natural gas or things that aren't connected with the biggest story in twenty years, maybe longer. This is a big deal and it's going to be going on—I swear to God I'm going to retire on this story, because it's just going to keep happening.

Saturday, November 28, 2009

No Islamo-terrorism to see here, just another ordinary day....

He's not an Arab or a Muslim, so nothing to see here. Just keep walking. Chalk it up to drugs, m'kay? Go about your business, America.

November 26, 2009 | Associated Press

Friday, November 27, 2009

Germany's top general resigns over Afghan coverup

Can you imagine Gen. Petraeus, McChrystal or somebody from the Joint Chiefs resigning over a U.S. military coverup of civilian deaths in Afghanistan or Iraq? Can you imagine, first, the U.S. mainstream media reporting on it, and second, even if they did, the American public even caring about it? Never.

For the record, the 30-40 civilians deaths in the scandalous coverup in question were caused by a U.S. airstrike -- but it was ordered by the German Bundeswehr under the NATO operational umbrella. Note how none of us in America were even made aware of this deadly mistake!

It's interesting -- and heartening -- that the German people are so concerned about the fate of innocent civilians in war. What did Germans learn from WWII that we didn't?

Germany's Top Soldier Resigns over Air Strike Accusations

Germany's highest-ranking soldier has resigned over allegations that the Defense Ministry did not come clean about civilians killed in a recent air strike in Afghanistan. Former Defense Minister Franz Josef Jung is also under pressure to resign.

Germany's highest-ranking soldier has resigned over allegations that the Defense Ministry did not come clean about civilians killed in a recent air strike in Afghanistan. Former Defense Minister Franz Josef Jung is also under pressure to resign.

November 26, 2009 | Speigel Online

URL: http://www.spiegel.de/international/germany/0,1518,663582,00.html

Obama's emissions targets not so costly after all?

So, estimates of the cost of Obama's goal to reduce CO2 emissions by 17% below 2005 levels vary from -$40 a year for an average family of four, to $1,539 per year by 2020. It all depends on who's doing the estimating. Conservatives will say that the EPA and the CBO harbor a dastardly liberal agenda so their estimates can't be trusted; liberals will say that Big Business is only looking out for itself, and scaring up some big numbers.

Personally, I would go with the CBO's numbers: the poorest households would save $40 per year; while the richest households would see an increased cost of $245 a year. In either case, emissions reductions would hardly cause the sky to fall on consumers' heads.

What we should not forget in all of this is that (1) reducing CO2 is a good thing, no matter what, because emissions are waste which equals inefficiency, both physical and economic, and (2) there is the untold health/human cost of greenhouse gases (aka air pollution) which increases heart and lung disease. Less CO2 in our atmosphere could save thousands of U.S. lives a year.

By Seth Borenstein

November 26, 2009 | Associated Press

More good military news: Divorce rates higher than ever

So we've got a record number of Army suicides this year, a record number of military PTSD cases, and now a record-high divorce rate.

Are you starting to get the picture? The War on Terra is killing our armed forces.

Military divorces edge up again in 9th year of war

By Pauline Jelinek

November 27, 2009 | Associated Press

Reagan not Reagany enough for pro-Reagan RNC?

Hey, seriously though, I've got a bunch of great, original campaign slogans for the RNC, which sees a sure-fire winner in resurrecting Reagan from his eternal infernal torment:

- "Where's the Reagan?"

- "A Reagan is forever."

- "Obama: The un-Reagan."

- "Got Reagan?"

- "Think outside the Reagan."

- "They're R-r-r-eagan!"

- "The few, the proud, the Reagans. (Except Ron, Jr.)"

- "Yo quiero Reagan."

- "We make Reagan the old-fashioned way -- We Reagan it."

- "Don't get mad. Get Reagan."

- "(Reagan) Lifts and separates."

- "Get a piece of the Reagan."

- "Leave the Reagan-ing to us."

- "Reagans wanted."

- "(Reagan) The king of presidents."

- "When it absolutely, positively has to be Reagan."

- "Once you Reagan, you can't stop."

- "Did somebody say Reagan?"

- "It's not your father's Reagan."

- "Reagan's number two; he tries harder."

- "Is it live, or is it Reagan?"

- "I'm Reagan, and I can't get up!"

By John Nichols

November 25, 2009 | The Nation

The most rigidly conservative members of the Republican National Committee are circulating a proposal to establish a purity test for the party's candidates.

If adopted, the party would withhold money from any contender who disagreed with conservative principles on more than two of 10 essential issues identified by the right-wingers.

"The problem is that conservatives have lost trust in the Republican Party that we will govern as conservatives," argues James Bopp Jr., an RNC member from Indiana who has spearheaded the purity-test push. "I think that loss of trust is warranted to a certain extent because of the fact that we in the final several years of the Bush administration were supporting increased government, earmarks and, ultimately, bailouts."

Earlier this year, Bopp and his compatriots pressured RNC chair Michael Steele to declare President Obama to be a "socialist." The conservative crusaders were rebuffed then, but if they win approval for their purity test at the committee's winter meeting in January, the party will officially express:

"Republican solidarity in opposition to Obama's socialist agenda is necessary to preserve the security of our country, our economic and political freedoms, and our way of life."

"Republican solidarity in opposition to Obama's socialist agenda is necessary to preserve the security of our country, our economic and political freedoms, and our way of life."

With Orwellian irony, Bopp and his buddies have labeled their proposal: "Reagan's Unity Principle for Support of Candidates. "The relevant portion of the resolution reads:

WHEREAS, the Republican National Committee shares President Ronald Reagan's belief that the Republican Party should espouse conservative principles and public policies and welcome persons of diverse views; and WHEREAS, the Republican National Committee desires to implement President Reagan's Unity Principle for Support of Candidates; and WHEREAS, in addition to supporting candidates, the Republican National Committee provides financial support for Republican state and local parties for party building and federal election activities, which benefits all candidates and is not affected by this resolution; and THEREFORE BE IT RESOLVED, that the Republican National Committee identifies ten (10) key public policy positions for the 2010 election cycle, which the Republican National Committee expects its public officials and candidates to support: (1) We support smaller government, smaller national debt, lower deficits and lower taxes by opposing bills like Obama's "stimulus" bill; (2) We support market-based health care reform and oppose Obama-style government run healthcare; (3) We support market-based energy reforms by opposing cap and trade legislation; (4) We support workers' right to secret ballot by opposing card check; (5) We support legal immigration and assimilation into American society by opposing amnesty for illegal immigrants; (6) We support victory in Iraq and Afghanistan by supporting military-recommended troop surges; (7) We support containment of Iran and North Korea, particularly effective action to eliminate their nuclear weapons threat; (8) We support retention of the Defense of Marriage Act; (9) We support protecting the lives of vulnerable persons by opposing health care rationing, denial of health care and government funding of abortion; and (10) We support the right to keep and bear arms by opposing government restrictions on gun ownership; and be further RESOLVED, that a candidate who disagrees with three or more of the above stated public policy positions of the Republican National Committee, as identified by the voting record, public statements and/or signed questionnaire of the candidate, shall not be eligible for financial support and endorsement by the Republican National Committee; and be further RESOLVED, that upon the approval of this resolution the Republican National Committee shall deliver a copy of this resolution to each of Republican members of Congress, all Republican candidates for Congress, as they become known, and to each Republican state and territorial party office.

Fair enough.

So here's a question: Applying the standard established in the resolution – review of the candidate's official record, public statements and answers to questions – would Ronald Reagan pass the purity test?

Let's see:

(1) Deficit spending soared during Reagan's presidency.Strike one.

(2) As governor of California, Reagan oversaw the development of Medi-Cal, the nation's largest Medicaid program – expanding it to cover long-term care and developed massive new managed care systems. Strike two.

(3) As governor of California, Reagan Reagan established the Air Resources Board to battle California's smog problems and supported aggressive government intervention where the market had failed to protect the environment. As president, Reagan signed more wilderness protections laws – which restrict private-sector exploitation of natural resources – than any president in history. Strike three.

(4) Reagan was a former union president who campaigned against the Taft-Hartley Act and other restrictions of the right of unions to organize. Strike four.

(5) Reagan signed the Immigration Reform and Control Act of 1986, which granted amnesty to most undocumented workers who could prove they had been in the country continuously for the previous five years. After he finished his presidency, Reagan continues to speak out forcefully for immigration rights. Strike five.

(6) After the 1983 bombing of a Marine barracks in Beirut, Reagan was urged by some to surge more troops into the region. Instead, he ordered the Marines to begin withdrawal from Lebanon. Strike six.

(7) Reagan acknowledged that during his presidency the U.S.sold weapons to Iran. Strike seven.

(8) Reagan was the first president to invite an openly gay couple to spend the night in the White House and he famously argued that gays and lesbians should not be discriminated against in a 1978 television advertising campaign. Strike eight.

(9) Shortly after his inauguration as governor of California, Reagan signed into law the most liberal abortion statute of its day". Strike nine.

(10) Here's Reagan, in 1991, on gun control: "I support the Brady Bill, and I urge the Congress to enact it without further delay." Strike ten.

Of course it is true that Reagan, like John Kerry, was for some ideas before he was against them.

Reasonable people might debate the proper point at which to try and pin Reagan down.

But no reasonable person can suggest that Ronald Reagan would have met the eight out ten test the RNC right-wingers seek to apply – especially on hot-button issues such as gun control, gay rights and immigration.

Indeed, one of the favorites of the RNC's extreme conservatives, Florida U.S. Senate candidate Marco Rubio, recently declared that Reagan was wrong to support amnesty for undocumented immigrants.

And it is probably worth noting that, when Reagan was seeking the Republican nomination in 1980, conservatives Phil Crane and John Connolly suggested that "the Gipper" was an amiable fellow but just not pure enough. Crane positioned himself that year as as a pure conservative alternative to Reagan.

Crane, the purist, won 1.8 percent of the vote in the New Hampshire Republican primary and exited stage right.

Bailed-out AIG soaking poor rural Kentuckians

By Yasha Levine

November 26, 2009 | AlterNet

Thanks to AIG, some of the poorest residents of rural Kentucky learned you can always be made poorer by corporate villains.

ClimateGate! Gotcha! Ka-Pow!

I've taken some trouble to read up on this because it's being called "ClimateGate" by some, and allegedly proves a global scientific conspiracy to foist the myth of global warming on us lay people. According to the Wired article, the scandal is a lot of hot air. It's snippets taken from thousands of stolen e-mails and posted on the Internet totally out of context. Nobody so far at the Climate Research Unit in East Anglia is denying the e-mails' authenticity, however. They seem for real.

The Examiner article quotes many more e-mails, which don't look good, and talk about deleting things and playing with graphs, but... Honestly, none of this means much to me, even though I've taken two college statistics courses. I will say though that these guys would have to be pretty clueless fraudsters to put all their diabolical plans in e-mails.

At any rate, these e-mails are out there now and I'm sure global warming doubters will raise lots of questions in the coming weeks and months. As your loyal foil to the lazy MSM and anti-intellectual conservatives, I'll be following this story as it develops....

By Kim Zetter

November 20, 2009 | Wired

By Tony Hake

November 20, 2009 | Examiner.com

Tuesday, November 24, 2009

Taibbi: Palin is politics' first WWE star

I don't see much of the U.S. media besides what I choose to read, so I have to take Taibbi's word for it on the media coverage of Palin....

By Matt Taibbi

November 20, 2009 | True/Slant

"Obama knows the long odds against a right-wing populist winning the presidency, no matter how good she looks in a skirt or running clothes, brandishing a gun. He shouldn't be too cocky, however, because the death of the center is ultimately a problem for him and the whole country. If the Palinistas seize the GOP, they probably cannot take the White House. But their brand of no-prisoners partisanship sure can tie up Congress."

The really beautiful thing about the culture war, from an entertainment standpoint, is that it is fundamentally irresolvable. There isn't a concrete set of issues involved, where in theory both sides could give in a little and find middle ground, reach some sort of compromise.

That's because there are no issues at all. At the end of this decade what we call "politics" has devolved into a kind of ongoing, brainless soap opera about dueling cultural resentments and the really cool thing about it, if you're a TV news producer or a talk radio host, is that you can build the next day's news cycle meme around pretty much anything at all, no matter how irrelevant — like who's wearing a flag lapel pin and who isn't, who spent $150K worth of campaign funds on clothes and who didn't, who wore a t-shirt calling someone a cunt and who didn't, and who put a picture of a former Vice Presidential candidate in jogging shorts on his magazine cover (and who didn't).

It doesn't matter what the argument is about. What's important is that once the argument starts, the two sides will automatically coalesce around the various instant-cocoa talking points and scream at each other until they're blue in the face, or until the next argument starts.

And while some of us are old enough to remember that once upon a time, these arguments always had at least some sort of ideological flavor to them, i.e. the throwdowns were at least rooted in some sort of real political issue (war, taxes, immigration, etc.) we've now got a whole generation that is accustomed to screaming at cultural enemies as an end in itself, for the sheer dismal fun of it. Start fighting first, figure out the reasons later.

Sarah Palin is the Empress-Queen of the screaming-for-screaming's sake generation. The people who dismiss her book Going Rogue as the petty, vindictive meanderings of a preening paranoiac with the IQ of a celery stalk completely miss the book's significance, because in some ways it's really a revolutionary and innovative piece of literature.

Palin — and there's just no way to deny this — is a supremely gifted politician. She has staked out, as her own personal political turf, the entire landscape of incoherent white American resentment. In this area she leaves even Rush Limbaugh in the dust.

The reason for that is that poor Rush is an anachronism, in the sense that his whole schtick revolves around talking about real political issues. And real political issues are boring.

Listen to Rush any day of the week and you'll hear him playing the old-fashioned pundit game: he goes about the dreary business of picking through the policies and positions and public statements of Democrats and poking holes in them, arguing with them, attacking them with numbers and facts and pseudo-facts and non-facts and whatever else he can get his hands on, honest or not, but at least he tries. The poor guy nearly killed himself this summer trying to find enough horseshit to arm himself with against the health care bill, coming up with various fairy tales about how state health agencies used death panels to try to kill cancer patients who just wanted to live a little longer, how section 1233 is Auschwitz all over again, yada yada yada.

Rush is no Einstein, but the man does research. It may be fallacious and completely dishonest research, but he does it all the same. His battlefield is world politics and most of the time the relevant action is taking place in Washington. As good as he is at what he does, he still has to travel to the action; he himself isn't the action.

Sarah Palin's battlefield, on the other hand, is whatever is happening five feet in front of her face. She is building a political career around the little interpersonal wars in the immediate airspace surrounding her sawdust-filled head. And in the process she connects with pissed-off, frightened, put-upon America on a plane that's far more elemental than the mega-ditto schtick.

Most normal people cannot connect on an emotional level with Rush's meanderings on how Harry Reid is buying off Mary Landrieu with pork in the health care bill. They can, however, connect with stories about how top McCain strategist and Karl Rove acolyte Steve Schmidt told poor Sarah to shut her pie-hole on election day, or how her supposed allies in the McCain campaign stabbed her in the back by leaking gossip about her to reporters, how Schmidt used the word "fuck" in front of her daughter, or even with the strange tales about Schmidt ordering Sarah to consult with a nutritionist to improve her campaign endurance when she herself knew she just needed to get out in the fresh air and run (If there's one thing Sarah Palin knows, it's herself!).

Complaining about the assholes we interact with on a daily basis is the #1 eternal pastime of the human race. We all do it, and we get to do it every day, because the world is full of assholes. Me personally, I waste an enormous amount of time seething over people who get onto crowded subway cars with big backpacks on and/or talk in the Amtrak quiet car and/or drive 57 mph in the fast lane or, my personal favorite, walking with glacial slowness in a horizontal row four overweight tourists across on a New York City sidewalk. We all get into furious arguments at work that make us want to explode in self-righteous fury (in my office dramas I always realize I was actually the asshole a day or so later) and when we get home from work, this is usually what our loved ones hear about for at least the first hour or so.

Not health care, not financial regulatory reform, not Iraq or Afghanistan, but — assholes.

Sarah Palin is on an endless crusade against assholes. It's all she thinks about. She doesn't really have any political ideas, in the classic sense of the word — in fact the only thing resembling real political convictions in Going Rogue revolve around the Trans-Alaska pipeline and how awesome she thinks it is.

Most of the rest of the book just catalogs her Gump-esque rise to national stardom (not having enough self-awareness to detect the monstrous narcissistic ambition that in reality was impelling her forward all along, she labors in the book to describe her various career leaps as lucky accidents or mystical acts of Providence) and the seemingly endless parade of meanies bent on tripping her up along the way. The book is really about her battles with these people, how much they did and do suck, and how difficult and inherently unfair life is for a decent hardworking American gal who just wants to live life, serve God, and try to be president without being bothered all the time.

Viewed through the prism of this particular brand of insanity (Palinsanity? does that work?), Katie Couric's notorious Palin interview last year really was a cheap shot. After all, Katie was trying to nail Palin — which is mean! Who among us can't sympathize with the experience of being sandbagged by some slick professional rival who catches you in a moment of weakness and, instead of lending a helping hand, drives a fireplace poker through your eye?

You'd have to be thinking about the broader picture, about the fact that the president of the United States ought not to be a drooling yahoo whose two favorite Supreme Court cases are Roe v. Wade and Roe v. Wade and who thinks living near Canada counts as foreign policy experience, to not see what an asshole Katie Couric was being. And that other reality, the reality where one worries about a national political candidate having the brains of an innertube, is less immediate than the five-foot airspace radius around the Palin bobblehead. It's harder for the average person to connect with, I guess.

Palin's extraordinary ability to inspire major national controversies around these injustices done to her immediate person is going to guarantee her some kind of major role in American politics for the next dozen years. In this regard she is going to have a willing ally in her supposed keen enemy, the mainstream media, which likewise loves nothing more than a political narrative that has nothing to do with politics. It'll be a virtually endless war over nonsense like this latest Newsweek cover, which hilariously is being seen as one or the other of a) a liberal media plot or b) a sexist assault on a prominent female politician by the male-dominated media world when in fact, as all of us in this dying print media business know, the magazine's motive was grounded entirely in the nihilistic desperation to sell newsstand copies.

And Sarah Palin sells copies. She is the country's first WWE politician — a cartoon combatant who inspires stadiums full of frustrated middle American followers who will cheer for her against whichever villain they trot out, be it Newsweek, Barack Obama, Katie Couric, Steve Schmidt, the Mad Russian, Randy Orton or whoever. Her followers will not know that she is the perfect patsy for our system, designed as it is to channel popular anger in any direction but a useful one, and to keep the public tied up endlessly in pointless media melees over meaningless nonsense (melees of the sort that develop organically around Palin everywhere she goes). Like George W. Bush, even Palin herself doesn't know this, another reason she's such a perfect political tool.

With Going Rogue, the 2012 reality show has already begun. As brainless political theater, she can't be topped. It's just too bad for conservatives that she happens to be unsustainably divisive and, as Newsweek points out, a really good bet to permanently marginalize the Republican party by reducing it to a pissed-off, semi-coherent mob that repulses independent voters on a visceral level. To paraphrase John Doman's Deputy Ops Rawls character from The Wire, she's "brilliant — fuckin' shame it's gonna end our careers, but still."

Ex-Scotland Yard cop turned Birther leader

It's ironic that two of the leading kooks in the Birther movement are naturalized U.S. citizens, one from Israel by way of Moldova, and another from Britain, both of whom settled in California. (Is it something in the water there?) Bizarre.

The former British police officer who wants to bring down Barack Obama

Conspiracist prominent in movement claiming president is an imposter

By Ed Pilkington

November 23, 2009 | The Guardian

November 23, 2009 | The Guardian

Neil Sankey has spent his life investigating organised crimes. As a former British police officer with almost 20 years experience, he was seconded to elite units of Scotland Yard through most of the 1970s and now runs his own private detective agency [http://www.privateinvestigation.com/] in California.

Over the years he has been involved in some big investigations. As part of the Special Branch and Bomb Squad he monitored British leftwing groups and the IRA, and in America his clients have included several big car companies.

But never has he handled anything quite as monumental as the investigation that is absorbing his energies today.

Sankey is pursuing what he believes to be fraud on a gigantic scale ? a conspiracy, no less, to infiltrate and destroy the free world by putting a foreign imposter into the White House.

Sankey is a member of the fringe alliance known widely as the Birthers (he dislikes the expression, considering it pejorative). Together with other activists, he seeks to prove that Barack Obama is not a true American and is therefore ineligible to be president.

Over the past year Sankey has been at the centre of some of the most aggressive efforts by the Birthers to unseat the president. At the end of last year he tried to block Obama's inauguration by contacting all 538 electoral college representatives who formally elect the president. More recently, he has carried out his own probe into Obama's personal identification history which has revealed, he believes, a suspicious multiplicity of social security numbers.

Sankey says his fascination began with the realisation "that this man wasn't what he said he was. He wasn't an ordinary Democrat ? he was far more extreme than that." So about a year ago he began reading blogs and websites that claimed to expose Obama's foreign roots, his spurious Hawaiian birth certificate and the $2m White House cover-up that has prevented the public finding out about the plot.

His travels put him in touch with Orly Taitz [http://www.orlytaitzesq.com/], one of the most energetic and flamboyant of the Birther leaders. Of Moldovan extraction, she emigrated via Israel to California where she works as a dentist and lawyer. She has filed numerous legal suits around the country on behalf of serving US military personnel attempting to prevent their deployments to Iraq and Afghanistan on the grounds that they should not be taking orders from an illegally serving commander-in-chief.

Sankey's journey from having worked in some of the most elite police units in Britain to taking part in a movement dedicated to the pursuit of a paranoid conspiracy theory may seem bizarre. But he insists it has been a natural progression. He joined the Hampshire force in 1961, and was seconded as a detective sergeant to Scotland Yard where he developed a specialism tracking leftwing political groups and the IRA.

"We created an operation into what we called revolutionary criminality ? monitoring leftwing bookshops and extremist literature, following the leftist fringe and the Marxist links of the IRA."

In 1980 he moved to California, set up his agency, and became a naturalised American in 1985.

Sankey contends that his police experience in England now informs his fight against Obama. "It's quite obvious to me - America is heading towards a socialised state just as has happened in Europe. Socialised medicine, everyone on the dole, and when everything collapses you tip the scales into Marxism."

He also believes his training in Scotland Yard is now reaping benefits for the Birthers. The same techniques he used to analyse the IRA's associations he is now applying to Obama. Most recently, he carried out an exhaustive search of databases that he claims threw up 140 different identification numbers and addresses for "Barack Obama". He admits the findings prove nothing ? there is nothing to link the entries to the president ? but he believes it raises further doubts that need investigating.

Taitz says Sankey's UK police expertise has been invaluable. "He has had superb training. I have the greatest respect for Scotland Yard."

The Birther movement is not a unique phenomenon within US politics. Bill Clinton was accused by conspiracy theorists of having murdered his friend and White House legal adviser Vince Foster; George Bush had to contend with the Truthers who believe he was the mastermind behind the 9/11 attacks.

But the Birthers are unlike previous movements in that they are focused on who Obama is rather than what he does.

"There is no other president who has had his citizenship questioned in this way," says Patricia Turner, an expert in folklore at the University of California, Davis. Turner says that the popular Birther theories that Obama has used fake Hawaiian documents to disguise the fact he was born in Kenya or Indonesia are retellings of an old story. "This is just a proxy for old-fashioned racism. They are driven by hostility towards anything they see as foreign or exotic."

Although the Birthers are on the fringe of American politics, they are part of a wider surge of rightwing anger towards Obama's perceived socialist policies that is sweeping the country.

As such they can command considerable support. An internet petition [http://www.wnd.com/index.php?fa=PAGE.view&pageId=81550] demanding an official inquiry into Obama's origins has been signed by almost 500,000; critics say the number is inflated by multiple clicks.

Like any virulent conspiracy theory, that of Obama's birth has proved immune to the intervention of fact. When Obama's birth certificate in Hawaii was digitally scanned for all to see, it was denounced as a forgery. The birth notices printed by two Hawaii newspapers announcing his birth in August 1961 were similarly dismissed.

Dozens of legal actions have been brought before the courts by Taitz and other Birther leaders, and so far every one has been thrown out. Last month a federal judge dismissed Taitz's lawsuit seeking to challenge the chain of military command up to Obama as commander-in-chief. In a devastating ruling, the judge accused Taitz of trying to "emasculate the military" in a way that would "leave this country defenceless".

None of these setbacks have dissuaded Sankey. He says accusations of racism are smears that he has come to expect. "The objection is not Obama's colour but his politics. I like him as a person, I just wish he was genuine."

[Yeah, Sankey likes Obama, he just believes Obama's a crypto-Marxist bent on destroying America. What's not to like? Jeeez. - J]

Sunday, November 22, 2009

Teabaggers feuding, heading toward the end

Here's my prediction: If the GOP can't find a way to control and use the Tea Party movement for all it's worth to them, they'll let it break into pieces and fade away.

On their own, I don't believe the teabaggers have staying power. Their biggest rallying cry was a one-time (maybe two-time, if we're lucky) stimulus package designed to fight a once-in-a-lifetime economic recession. If they can't agree on what they're for and against, what they want, and how they're going to organize and fund themselves -- basic instiutional questions for any going concern -- then their days are numbered.

By Kenneth P. Vogel

November 20, 2009 | Politico

Economists agree stimulus was too small, but worth it

New Consensus Sees Stimulus Package as Worthy Step

By Jackie Calmes and Michael Cooper

November 20, 2009 | New York Times

By Jackie Calmes and Michael Cooper

November 20, 2009 | New York Times

Now that unemployment has topped 10 percent, some liberal-leaning economists see confirmation of their warnings that the $787 billion stimulus package President Obama signed into law last February was way too small. The economy needs a second big infusion, they say.

Jalin Willis checked the job listings in Denver last month. The nation's unemployment rate topped 10 percent this month.

No, some conservative-leaning economists counter, we were right: The package has been wasteful, ineffectual and even harmful to the extent that it adds to the nation's debt and crowds out private-sector borrowing.

These long-running arguments have flared now that the White House and Congressional leaders are talking about a new "jobs bill." But with roughly a quarter of the stimulus money out the door after nine months, the accumulation of hard data and real-life experience has allowed more dispassionate analysts to reach a consensus that the stimulus package, messy as it is, is working.

The legislation, a variety of economists say, is helping an economy in free fall a year ago to grow again and shed fewer jobs than it otherwise would. Mr. Obama's promise to "save or create" about 3.5 million jobs by the end of 2010 is roughly on track, though far more jobs are being saved than created, especially among states and cities using their money to avoid cutting teachers, police officers and other workers.

"It was worth doing — it's made a difference," said Nigel Gault, chief economist at IHS Global Insight, a financial forecasting and analysis group based in Lexington, Mass.

Mr. Gault added: "I don't think it's right to look at it by saying, 'Well, the economy is still doing extremely badly, therefore the stimulus didn't work.' I'm afraid the answer is, yes, we did badly but we would have done even worse without the stimulus."

In interviews, a broad range of economists said the White House and Congress were right to structure the package as a mix of tax cuts and spending, rather than just tax cuts as Republicans prefer or just spending as many Democrats do. And it is fortuitous, many say, that the money gets doled out over two years — longer for major construction — considering the probable length of the "jobless recovery" under way as wary employers hold off on new hiring.

But there are criticisms, mainly that the Obama team relied last winter on overly optimistic economic assumptions and oversold the job-creating benefits of the stimulus package.

Optimistic assumptions in turn contributed to producing a package that if anything is too small, analysts say. "The economy was weaker than we thought at the time, so maybe in retrospect we could have used a little bit more and little bit more front-loaded," said Joel Prakken, chairman of Macroeconomic Advisers, another financial analysis group, in St. Louis.

While some conservatives remain as skeptical as ever that big increases in government spending give the economy a jolt that is worth the cost, Martin Feldstein, a conservative Harvard economist who served in the Reagan administration, said the problem with the package was that some of its tax cuts and spending programs were of a variety that did little to spur the economy.

"There should have been more direct federal spending that would have added to aggregate demand," he said. "Temporary tax cuts and one-time transfers to seniors were largely saved and didn't stimulate spending."

Even the $787 billion price tag overstates the plan's stimulus value given changes made in Congress, economists say. Nearly a tenth of the package, $70 billion, comes from a provision adjusting the alternative minimum tax so it does not hit middle-income taxpayers this year. That routine fix, which would do nothing to stimulate the economy, was added in part to seek Republican votes. But to keep the package's overall cost down, provisions that would stimulate the economy — like aid to revenue-starved states and infrastructure projects — got less as a result.

Among Democrats in the White House and Congress, "there was a considerable amount of hand-wringing that it was too small, and I sympathized with that argument," said Mark Zandi, chief economist of Moody's Economy.com and an occasional adviser to lawmakers.

Even so, "the stimulus is doing what it was supposed to do — it is contributing to ending the recession," he added, citing the economy's third-quarter expansion by a 3.5 percent seasonally adjusted annual rate. "In my view, without the stimulus, G.D.P. would still be negative and unemployment would be firmly over 11 percent. And there are a little over 1.1 million more jobs out there as of October than would have been out there without the stimulus."

Politically, however, the president is saddled with his original claim that, with the stimulus, the jobless rate would peak at 8.1 percent — a miscalculation that Republicans constantly recall. While the administration has said its economic assumptions were in line with private forecasts, most of which also underestimated the recession's punch, it was more optimistic than most.

"That was a mistake," said Jeffrey A. Frankel, a Harvard University economist and former Clinton administration official who is a member of the National Bureau of Economic Research panel that judges when recessions start and end. "I thought so at the time."

Christina D. Romer, chairwoman of Mr. Obama's Council of Economic Advisers, said attention to that too-rosy projection "prevents people from focusing on the positive impact of the fiscal stimulus. So of course I find that frustrating."

Much federal infrastructure money has gone not to new job-creating projects but to finance existing plans, which otherwise would be unaffordable to states.

So the stimulus has not "supercharged" transportation construction as was hoped, said Charles Gallagher, an asphalt company owner, speaking for the American Road and Transportation Builders Association, but it has nonetheless been "a welcome Band-Aid" to offset state cuts.

"Many contractors across the nation have been able to sustain, if not add to, their work force," he said.

That sort of impact is what makes federal aid to state governments rank high in economists' reckoning of the stimulus value of various proposals. Every dollar of additional infrastructure spending means $1.57 in economic activity, according to Moody's, and general aid to states carries a $1.41 "bang" for each federal buck.

Even more effective are increases for food stamps ($1.74) and unemployment checks ($1.61), because recipients quickly spend their benefits on goods and services.

By contrast, most temporary tax cuts cost more than the stimulus they provide, according to research by Moody's. That is true of two tax breaks in the stimulus law that Congress, pressed by industry lobbyists, recently extended and sweetened — a tax credit for homebuyers (90 cents of stimulus for each dollar of tax subsidy) and extra deductions for businesses' net operating losses (21 cents).

Economists said Republicans' recent proposals to rescind unspent money would be a mistake.

James Glassman, a senior economist at JPMorgan Chase & Company, said: "If we could be absolutely convinced that the growth we're getting is for reasons beyond the help the government is giving, then that would make sense. But the fact is we can't be certain of that."

Saturday, November 21, 2009

Poll: 26 percent of Americans self-identify as kooks

Ab-so-lute-ly amazing.

In U.S. politics, it's not the Smarts vs. the Stupids anymore, not like it used to be. It's now the Sane vs. the Crazy. And crazy people apparently now make up 26 percent of the population. (This is making me start to think maybe the 2nd Amendment isn't such a bad idea.... How will I possibly defend myself and my loved ones when those 60 million rabid Republizombies come to storm my house and consume our living flesh?)

As you all know, it's crazy to attempt to argue with a crazy person. So we sane people basically have 3 options in dealing with them: (1) smile compassionately and pay lip service to the legitimacy of their delusions to spare them psychological stress and unpleasant emotions, (2) safely steer clear and ignore them, or (3) have them committed for their and society's good. I leave it to you, my fellow Sane Americans, to decide.

Oh, and if you hear about any teabaggers starting to bite people, let me know so I can immediately head to the nearest gun shop.

By Eric Kleefeld

November 19, 2009 | TPMDC

November 19, 2009 | TPMDC

The new national poll from Public Policy Polling (D) has an astonishing number about paranoia among the GOP base: Republicans do not think President Obama actually won the 2008 election -- instead, ACORN stole it.

This number goes a long way towards explaining the anger of the Tea Party crowd. They not only think Obama's agenda is against America, but they don't think he was actually the choice of the American people at all! Interestingly, NY-23 Conservative candidate Doug Hoffman is now accusing ACORN of stealing his race, and Fox News personalities have often speculated about ACORN stealing the 2008 Minnesota Senate race for Al Franken.

The poll asked this question: "Do you think that Barack Obama legitimately won the Presidential election last year, or do you think that ACORN stole it for him?" The overall top-line is legitimately won 62%, ACORN stole it 26%.

Among Republicans, however, only 27% say Obama actually won the race, with 52% -- an outright majority -- saying that ACORN stole it, and 21% are undecided. Among McCain voters, the breakdown is 31%-49%-20%. By comparison, independents weigh in at 72%-18%-10%, and Democrats are 86%-9%-4%.

Now, the obvious comparison would be that many Democrats felt that George W. Bush didn't legitimately win the 2000 election. But there are some clear differences.

First of all, Al Gore empirically won the national popular vote in 2000, and lost in a disputed recount process in Florida. By comparison, John McCain lost the national popular vote by a 53%-46% margin.

In order to believe that Obama wasn't the true winner of the 2008 election, one would have to think that ACORN (and perhaps other groups) stuffed ballots to the tune of over 9.5 million votes, Obama's national margin.

PPP communications director Tom Jensen says: "Belief in the ACORN conspiracy theory is even higher among GOP partisans than the birther one, which only 42% of Republicans expressed agreement with on our national survey in September."

Wednesday, November 18, 2009

Sarah won't rule out a Palin-Beck ticket, you betcha!

Palin won't rule out running with a dancing chimp either.

Seriously though, this just confirms everything I've been saying about the long, downward slide of the GOP. Its leadership is coming from un-elected, unaffiliated "rogues" and rightwing bloviators on FOX and talk radio. It's sad to see a once proud party reduced to this.

It's no secret that former GOP vice-presidential candidate Sarah Palin and Fox News host Glenn Beck share great respect and admiration — so their fans can be forgiven for wondering: Is a "dream ticket" of Palin-Beck ticket completely out of the question?

Perhaps not.

Palin initially chuckled when Newsmax broached the idea. But then she had some serious words of praise for the popular Fox personality.

"I can envision a couple of different combinations, if ever I were to be in a position to really even seriously consider running for anything in the future, and I'm not there yet," Palin tells Newsmax. "But Glenn Beck I have great respect for. He's a hoot. He gets his message across in such a clever way. And he's so bold — I have to respect that. He calls it like he sees it, and he's very, very, very effective."

[Yeah, he's very effective at self-promotion, a quality which Palin surely admires. - J]

[Yeah, he's very effective at self-promotion, a quality which Palin surely admires. - J]

BCBS denies boy new prosthetic arm

Hey, kid, life's tough. It's unfair. But you were born with only one arm, so I guess you kinda know that already....

Anyway, nobody owes you a prosthetic arm. You see, it's all about the free market for health care and private insurance and supply and demand. It's what makes America great. It's all very hard for you to understand right now, but when you grow up to be a one-armed man, you'll get it.

In the meantime, don't blame the insurance companies. They gotta feed their kids, too. And hey, your other arm looks pretty darn strong! Look out! Attaboy, tiger! Now run along and play.

By Danielle Ivory

November 17, 2009 | Huffington Post Investigative Fund

Tuesday, November 17, 2009

Another year, another record for Army suicides

Oh my, Lib'rul Media, you aint what you used to be. Look at you, ignoring the elephant in the room.

Here CNN writes about record numbers of army suicides and drug abusers, but conveniently fails to mention that they're being deployed to s***holes Afghanistan and Iraq over and over again. CNN doesn't even speculate why so many soldiers are killing themselves. Likewise, the Army is officially baffled. I guess CNN considers it a big, unsolvable mystery, too. Anyway, I bet the solution is more frequent psychiatric testing and counseling. Yeah, that's the ticket.

By Mike Mount

November 18, 2009 | CNN

November 18, 2009 | CNN

Suicides among soldiers this year have topped last year's record-breaking numbers, but Army officials maintain a recent trend downward could mean the service is making headway on its programs designed to reduce the problem, Army officials said Tuesday.

Since January, 140 active-duty soldiers have killed themselves while another 71 Army Reserve and National Guard soldiers killed themselves in the same time period, totaling 211 as of Tuesday, Gen. Peter Chiarelli, U.S. Army vice chief of staff, told reporters at a briefing Tuesday.

But he said the monthly numbers are starting to slow down as the year nears its end.

"This is horrible, and I do not want to downplay the significance of these numbers in any way," Chiarelli said.

For all of 2008, the Army said 140 active-duty soldiers killed themselves while 57 Guard and Reserve soldiers committed suicide, totaling 197, according to Army statistics.

The Army is still trying to tackle why soldiers are killing themselves.

[If the Army's cluelessness doesn't undermine your faith in their intelligence, then I don't know what will. But of course they know why. They just can't say it. - J]

"We still haven't found any statistically significant causal linkage that would allow us to effectively predict human behavior. The reality is, there is no simple answer -- each suicide case is as unique as the individuals themselves," Chiarelli said.

He also said there were troubling new statistics showing an increase in suicide rates among young soldiers who have never deployed, another factor puzzling Army researchers.

To add to the Army's problems, Chiarelli said there is a rise in numbers of soldiers abusing prescription drugs and alcohol upon returning from the war zones.

But Chiarelli said the news was not all grim.

"I do believe we are finally beginning to see progress being made," he said referring to a downward trend in suicide numbers in recent months. "The general trend line with the exception of a couple of months has been down."

"We attribute this reduction in the number of suicides to the many actions we have taken since February to inform and educate leaders and soldiers on this important issue," Chiarelli said.

Since March, the Army has implemented numerous programs and policies in an attempt to quickly slow the rate. Programs range from a suicide prevention task force to a day off from official duties to focus on suicide prevention. The service has implemented what it calls a Comprehensive Soldier Fitness Program, giving every soldier a mental assessment twice a year in the same style the Army tests soldiers for fitness.

"It gives the same emphasis to psychological, emotional and mental strength that we have previously given to physical strength," Chiarelli said.

The Army also has tested a program that gave mental-health evaluations to a group soldiers returning from the war zone. Some were treated face-to-face with mental-health providers while others were treated online by providers.

Chiarelli said the initial results were promising, and doctors said they could have great success treating patients online.

The test seems to give the Army some answers on how to treat the variety of soldiers from young to old.

"Younger soldiers prefer the online method of evaluation more than they do the face-to-face, and older soldiers -- some of you might not find this so surprising -- find face-to-face more to their liking," according to the general.

Chiarelli also gave examples of Army bases that seem to have shown improvement in suicide warning signs and prevention this year resulting in decreased number of suicide rates, including Fort Hood in Texas, Fort Bragg in North Carolina and Fort Drum in New York.

Fort Bragg has had six suicides to date, Fort Hood has had two and Fort Hood has had 11, but it is the largest U.S. military base with 60,000 troops.

There are Army posts, however, that were not showing signs of improvement.

"We are very concerned with the increase this year of suicide at Fort Campbell, Fort Stewart and Schofield Barracks," Chiarelli said.

Fort Campbell, in Kentucky, has had 18 suicides so far this year, with 11 of them occurring in the first quarter of 2009. Fort Stewart in Georgia has had 10 deaths, six of them occurring over the first five months of the year. And Schofield Barracks in Hawaii has had seven deaths.

All of the bases Chiarelli mentioned have different populations and deployment levels and reflect different suicide rates and ratios.

Chiarelli stressed his frustration with getting answers to the suicide problem.

"Everywhere I try to cut this and look at it to try to find out what the causal effect is, I get thwarted. And that's why we think that we've got to look in its totality at a whole bunch of different issues, and it's going to take time," he said.

Subscribe to:

Posts (Atom)